In joint-ownership businesses—whether family enterprises, startups, or partnerships—the unexpected death, disability, or departure of a co-owner can imperil continuity. A Business Value Protection Trust (BVPT) provides pre-funded liquidity and a clear exit mechanism, preserving both business stability and family harmony.

What Is a Business Value Protection Trust?

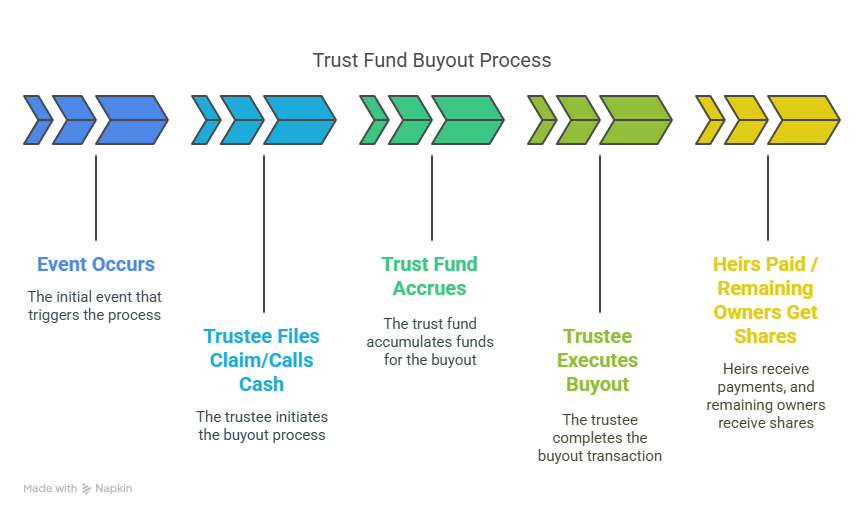

A BVPT is a dedicated trust into which co-owners allocate the right to purchase departing partners’ shares upon specified trigger events. Funded through insurance, cash, or disability cover, the trust empowers a neutral trustee to execute buyouts swiftly and fairly.

Key Benefits:

- Immediate Liquidity: Prevents forced asset sales or taking on high-interest debt.

- Dispute Avoidance: Pre-agreed valuation and terms eliminate ambiguity.

- Continuity of Control: Remaining owners retain seamless operational command.

- Family Protection: Outgoing owner’s heirs receive equitable compensation without negotiations.

Real-World Mini Case: Pune Garment Exporter

Scenario: A four-partner garment exporting firm in Pune faced turmoil when Partner A passed away unexpectedly. No BVPT was in place, forcing the remaining partners to scramble for funds—ultimately selling business equipment at a 20% discount.

BVPT Solution (Hypothetical):

- Policy Funding: ₹5 crore term policy on each partner.

- Trigger: Death or permanent disability.

- Outcome: On Partner A’s death, the trust would have made ₹4.8 crore (after 4% claim costs) available within 10 days, funding a fair buyout and avoiding asset distress.

Step-by-Step Setup Guide

Step 1: Agree on Valuation Method

- Choose EBITDA multiple, book value, or DCF.

- Schedule revaluations (e.g., annually).

Step 2: Fund the Purchase Price

- Life Insurance: Term or whole-life sized to valuation.

- Cash Contributions: Lump-sum or installments.

- Disability Cover: Ensures buyout if an owner becomes incapacitated.

Step 3: Define Trigger Events

- Death or total permanent disability.

- Retirement, resignation, or critical illness.

- Contractual breaches or other agreed circumstances.

Step 4: Execute Core Documents

- Buy-Sell Agreement: Specifies valuation, funding, and trigger conditions.

- Trust Deed: Establishes the BVPT, trustee powers, and payout instructions.

- Power of Attorney: Grants trustee authority to transfer shares on triggers.

Quantified Impact

- Speed: 7–10 days claim settlement vs. 3–6 months of court-led transfer.

- Cost Efficiency: Avoids 15–25% losses from fire-sale asset divestments.

- Tax Neutrality: Insurance proceeds are tax-free if premiums paid by partners, and trust distributions can be optimized under the Income Tax Act.

Regulatory & Compliance Notes (India)

- IRDAI Guidelines: Assignment of policy to trust must comply with Form S9 and insurer notification.

- FEMA Considerations: For NRI partners, trust-owned policies must adhere to foreign exchange regulations.

- Stamp Duty & GST: Trust deeds may attract stamp duty; insurance premiums are subject to GST as applicable.

Why You Need a BVPT Today

A BVPT turns uncertainty into a structured plan—ensuring your business weathers leadership changes, personal crises, and life’s unpredictability. For HNIs, CEOs, and family businesses, it’s the cornerstone of robust succession planning.

Ready to set up your Business Value Protection Trust?

Schedule your strategy session today.