Continuity Capital Review for Business Families

A product-neutral review of how the family will access capital when continuity is tested.

A business family may have substantial wealth, valuable assets, strong businesses, trusted advisors, and clear intentions.

But during transition, the real question is not only: “What does the family own?”

The sharper question is: “What capital will be available, for whom, when, and without disturbing control, forcing asset sale, or creating family pressure?”

The Continuity Capital Review helps business families examine whether liquidity is properly designed before succession, incapacity, death, partner exit, estate equalization, debt pressure, trust funding, or family settlement creates urgency.

Product-neutral. Advisor-coordinated. Designed for serious families where liquidity, control, and continuity must work together.

Private-office note:

This review is conducted discreetly and selectively. Families may share only broad context at the first stage. Specific family, legal, ownership, or financial details should be discussed privately only where the matter is suitable for structured review.

The Asset-Rich, Liquidity-Poor Family

The estate may be valuable. But can it produce usable capital when the family needs it?

A business family may own a strong company, valuable real estate, promoter holdings, long-term investments, and family assets.

On paper, the family may look financially secure.

Then transition happens.

A spouse needs security. One child needs to continue the business. Another expects fairness. A loan or guarantee must be addressed. A trust or will must be implemented. Advisors need instructions.

But most of the wealth is locked inside assets that cannot be sold quickly, safely, or without consequences.

This is when families discover that net worth and usable capital are not the same.

They are asset-rich. But liquidity-poor. Well-advised in parts. But not always continuity-ready as one structure.

The Continuity Capital Review exists to identify this gap before the family is forced to decide under pressure.

Why Net Worth Is Not Usable Capital

Many families appear strong on paper. They may own real estate, promoter holdings, business equity, long-term investments, family assets, and operating companies.

But these assets may not be easy to use when the family needs capital quickly.

A property may be valuable but difficult to sell. A business may be profitable but not liquid. A holding may be significant but strategically important. A family may be asset-rich but cash-unprepared. A spouse may need security without disturbing ownership. One heir may need business control while another needs fair settlement. Trustees or executors may have responsibility but no practical liquidity.

Continuity capital exists for this reason.

It is not about buying a product first. It is about ensuring that capital is available at the right moment, in the right hands, for the right purpose.

A Continuity Capital Review may be relevant if:

- most family wealth is held in business, real estate, private company shares, promoter holdings, or other illiquid assets

- the founder or senior family member still controls major decisions

- the family has valuable assets but limited ready liquidity

- one child is active in the business and others are not

- estate equalization has not been clearly funded

- spouse security depends on future family cooperation

- loans, guarantees, or business obligations exist

- trusts, wills, nominations, or shareholder arrangements exist but liquidity has not been reviewed

- multiple advisors are involved but no one has mapped capital readiness

- the family assumes "something can be sold later" without testing timing, tax, control, and emotional consequences

The issue is not whether the family is wealthy. The issue is whether usable capital will be available, accessible, controlled, and properly aligned when continuity is tested.

The Central 30/90/180-Day Question

If transition created a capital need within 30, 90, or 180 days, where would the money come from?

And more importantly:

would it be available without selling strategic assets?

would it be accessible to the right person?

would it preserve family and business control?

would it avoid pressure across heirs or branches?

would it align with documents, tax, banking, and legal structures?

would it work if the founder was not available to decide?

A family may have wealth. But continuity depends on whether capital can move at the right time, through the right hands, for the right purpose.

Stakeholder Tension

For the founder, the question is: will the family remain in control if I am not available to decide?

For the spouse, the question is: will I have security without depending on hurried family decisions?

For the child in the business, the question is: can the enterprise continue without being weakened by settlement pressure?

For non-active heirs, the question is: will fairness be funded without forcing division of the wrong assets?

For advisors, the question is: is there one capital map connecting documents, tax, banking, ownership, and family intent?

What Families Often Assume vs What Transition May Reveal

Many families assume:

- wealth automatically creates liquidity

- a will automatically solves continuity

- business cash can be used if required

- property can be sold later

- heirs will agree when needed

- existing advisors will coordinate everything

- old policies, reserves, investments, or credit lines are still adequate

Transition may reveal:

- assets are valuable but not liquid

- liquidity exists but is not accessible to the right person

- documents exist but capital is not available

- heirs are equal on paper but not aligned in responsibility

- business funds cannot be freely withdrawn

- selling assets may damage control

- advisors are competent but not working from one continuity map

What Continuity Capital Protects

The purpose of continuity capital is not merely to create cash.

It may protect:

- family control

- business continuity

- spouse security

- fair settlement across heirs

- estate equalization

- trust funding

- debt and guarantee obligations

- partner or shareholder settlement

- family dignity during transition

- prevention of forced asset sale

- implementation of estate and succession plans

- advisor coordination during sensitive events

A family’s continuity plan may be well-intentioned. But if the capital required to execute it is not available, the plan may remain theoretical.

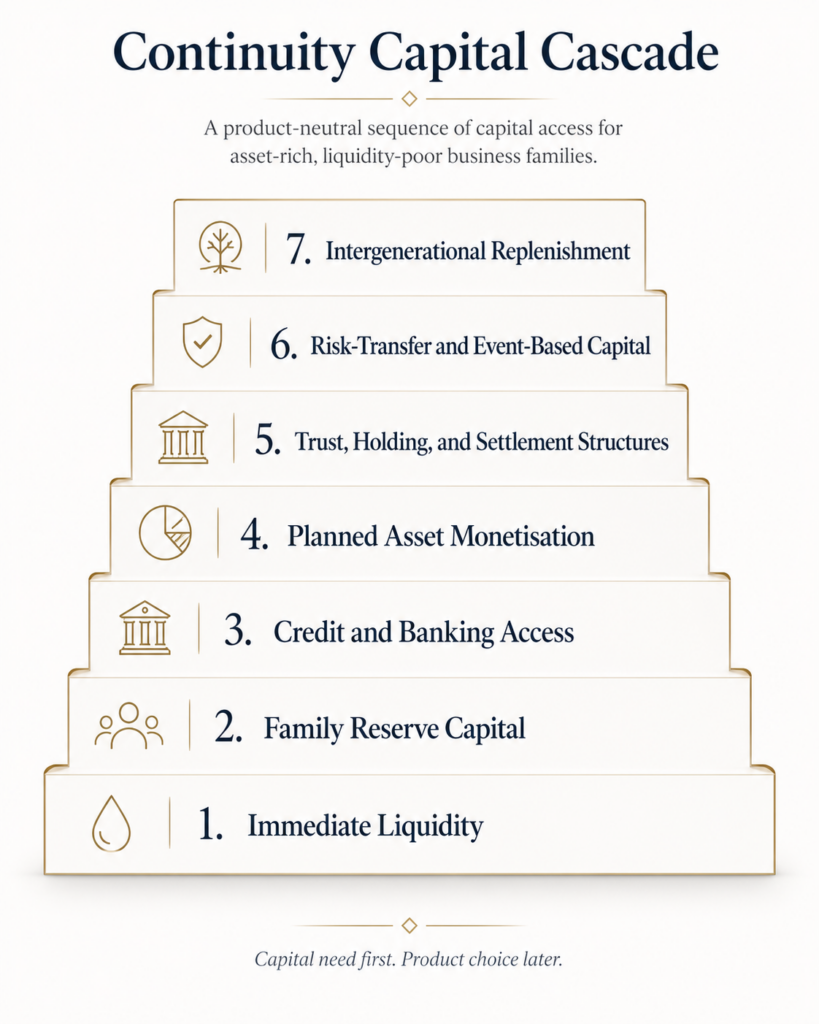

Continuity Capital Cascade Layers

Layer | Purpose | Possible Sources |

1. Immediate Liquidity | Urgent family, estate, business, or settlement needs. | Cash, liquid investments, emergency reserves, short-term accessible funds. |

2. Family Reserve Capital | Pre-planned liquidity pools so the family knows what can be used and who may authorize it. | Designated investment buckets, family reserves, business reserves. |

3. Credit and Banking Access | Bridge liquidity needs without immediate asset sale. | Overdrafts, credit lines, loan against securities, loan against property where suitable. |

4. Planned Asset Monetisation | Use assets without panic sale or control damage. | Pre-identified sale, refinance, or reorganization options. |

5. Trust, Holding, and Settlement Structures | Align liquidity with legal, ownership, and family intent. | Trust funding, family settlement pools, shareholder or partner arrangements. |

6. Risk-Transfer and Event-Based Capital | Create capital at a defined transition event. | Life insurance, key-person cover, buy-sell funding, business-continuity cover, other suitable risk-transfer tools. |

7. Intergenerational Replenishment | Restore reserves and capital systems for the next generation. | Replenishment rules, periodic review, governance decisions. |

Asset Value vs Asset Convertibility

A Continuity Capital Review separates asset value from asset usability.

Asset Type | Value May Be High | Liquidity May Be Weak | Continuity Issue |

Operating business | Yes | Often | Cannot sell or withdraw capital without affecting control and operations. |

Real estate | Yes | Often | Sale may be slow, tax-sensitive, or emotionally difficult. |

Promoter holdings | Yes | Sometimes | Sale or pledge may affect control or market perception. |

Private company shares | Yes | Often | Valuation and transfer may be complex. |

Jewellery / personal assets | Yes | Sometimes | May be family-sensitive and unsuitable for settlement. |

Long-term investments | Yes | Varies | Timing, tax, and market conditions must be reviewed. |

Insurance / risk-transfer assets | Depends | Event-based | Useful only where suitable and properly structured. |

Funding Methods That May Be Reviewed

A Continuity Capital Review does not begin with a product. It begins with the family’s capital requirement.

Depending on the family’s structure, continuity capital may be arranged through one or more methods. These may include:

- existing cash reserves

- liquid investments

- fixed-income allocations

- business reserves

- overdraft or bank credit facilities

- loan against suitable financial assets

- loan against property, where appropriate

- planned asset monetisation

- shareholder or partner funding arrangements

- trust funding structures

- family settlement pools

- key-person protection

- business-continuity cover

- life insurance for estate equalization or transition liquidity

- annuity or structured income arrangements

- risk-transfer tools

- other suitable liquidity or funding instruments

The appropriate method depends on timing, certainty, cost, tax treatment, legal ownership, family intent, control impact, advisor coordination, and implementation feasibility.

No instrument should be selected in isolation.

How Products and Instruments Fit

The review is product-neutral.

Life insurance, key-person cover, annuity or income-continuity structures, bank credit, asset-backed borrowing, reserves, investment liquidity, trust funding, or planned asset monetisation may all be relevant in different situations.

Life insurance is not introduced as a product-first discussion. It may be considered only where the continuity architecture reveals a legitimate funded-liquidity requirement.

In suitable cases, life insurance may help provide capital at a defined transition point without depending on asset sale, business cash flow, borrowing, or family negotiation under pressure.

But it is never the starting assumption.

The starting point is always: what continuity capital is required, and what is the most suitable way to fund it?

How Funding Methods Are Evaluated

Each funding method is reviewed against seven questions:

- Timing: Will the capital be available exactly when the family needs it?

- Certainty: Will the funding still work under stress, transition, incapacity, death, dispute, or market disruption?

- Control: Does the method preserve family control, business continuity, and ownership stability?

- Liquidity: Can the capital be accessed without delay, forced sale, or operational damage?

- Cost: Is the cost justified by the continuity risk being addressed?

- Tax and legal alignment: Does the method align with the family’s CA, lawyer, trustee, banker, and documentation structure?

- Family fairness: Does it reduce or increase pressure across heirs, branches, spouses, or successors?

A funding method that looks attractive in isolation may still be unsuitable if it weakens control, creates tax friction, complicates ownership, or increases family pressure.

If Continuity Capital Is Not Ready

The real cost is not only financial.

When continuity capital is not ready, the cost may appear as:

- a property sold at the wrong time

- business control diluted

- a spouse waiting for family agreement

- one child feeling burdened

- another child feeling unfairly treated

- bankers asking questions before the family is ready

- trustees unable to act smoothly

- advisors working from incomplete information

- family unity being tested by liquidity pressure

The family may still be wealthy. But it may not be ready.

Where Continuity Capital Is Usually Required

Continuity capital commonly becomes important in these situations:

- Estate equalization: when one heir may continue the business while others need fair treatment without weakening the enterprise.

- Founder dependency: when business value, banking relationships, client confidence, or decision authority still depend heavily on one person.

- Buy-sell or partner settlement: when a partner, shareholder, family branch, or business associate must be bought out or settled.

- Spouse security: when the spouse needs financial certainty without disrupting business control or children’s future ownership.

- Trust funding: when trust structures are intended but not yet funded adequately.

- Debt and guarantee exposure: when personal guarantees, loans, or business obligations could create pressure during transition.

- Business stabilization: when the company may need working capital or confidence capital after the founder or key person is unavailable.

- Forced-sale prevention: when important family assets should not be sold simply because liquidity was not arranged earlier.

How the Review Works

Step 1: Identify transition events. The review begins by identifying events that may create capital pressure: founder death, incapacity, succession, partner exit, family branch settlement, estate administration, trust activation, debt or guarantee pressure, business disruption, or family restructuring.

Step 2: Identify capital requirements. How much capital is required, by whom, when, and for what purpose?

Step 3: Review existing liquidity. Existing sources are reviewed first: cash, investments, business reserves, credit lines, asset-sale options, existing insurance, trust assets, and family liquidity arrangements.

Step 4: Identify the gap. The review clarifies what is unfunded, illiquid, inaccessible, poorly timed, legally misaligned, dependent on forced asset sale, or dependent on family agreement under pressure.

Step 5: Evaluate funding methods. Funding methods are reviewed product-neutrally. Existing liquidity, credit, restructuring, reserves, asset monetisation, insurance, income structures, trust funding, or other instruments may be considered depending on suitability.

Step 6: Coordinate implementation. Implementation must be aligned with the family’s CA, lawyer, banker, trustee, insurer, investment advisor, and family decision-makers.

Continuity capital is not only a financial decision. It is an implementation decision.

Family Liquidity Policy

A Continuity Capital Review may lead to a Family Liquidity Policy.

This policy may clarify:

- minimum liquid reserve

- business reserve rules

- what assets should not be sold under pressure

- who can approve use of family liquidity

- how spouse security will be funded

- how estate equalization will be funded

- how family branch settlements will be handled

- how trustees or executors access liquidity

- how credit lines may be used

- when insurance or other risk-transfer tools are suitable

- how often the liquidity position must be reviewed

Most advisors discuss products. Family-office-grade work creates policies, responsibilities, and review discipline.

Who Controls the Capital?

A family may have assets and even liquidity, but still face uncertainty if no one knows who can access or authorize it.

The review examines:

- who owns the liquidity

- who can authorize use

- who receives the capital

- whether the spouse can access it

- whether the business can use it

- whether trustees or executors can act

- whether bank mandates are updated

- whether nominations and ownership match intent

- whether family members understand the process

Liquidity without decision authority is still fragile.

Continuity Capital Gap

The review estimates the gap between:

Capital required during transition

minus

capital already available, accessible, controlled, and properly aligned.

The gap may need to be funded through reserves, credit, investment liquidity, asset monetisation, restructuring, insurance or other risk-transfer tools, trust funding, or staged family settlement.

This gap is where serious implementation begins.

Continuity Capital Stress Tests

The review may test scenarios such as:

- Founder unavailable for 90 days: Who signs? Who pays? Who speaks to bankers? What capital is available?

- Founder death: What capital reaches the spouse, business, estate, trust, or heirs without forced sale?

- One child active, one child inactive: How is fairness handled without weakening the business?

- Partner or shareholder exit: What funds the settlement?

- Debt or guarantee pressure: What happens if lenders require reassurance or repayment?

- Real estate-heavy estate: What funds the family before property can be sold, transferred, or divided?

- Trust activation: Does the trust have enough liquidity to function?

How This Connects to the Family Continuity Diagnostic

In most serious family situations, the Continuity Capital Review should follow a broader Family Continuity Diagnostic.

Why?

Because liquidity cannot be separated from ownership, control, succession, documents, tax considerations, trust structures, family expectations, business continuity, and advisor coordination.

The Family Continuity Diagnostic helps identify where continuity may fail.

The Continuity Capital Review then examines whether capital is available to support the architecture.

When Existing Arrangements Should Be Reviewed

Even where a family already has policies, investments, wills, trusts, nominations, credit lines, or liquidity arrangements, continuity capital should be reviewed periodically.

Existing arrangements may need review when:

- family wealth has grown materially

- business value has increased

- new properties, companies, trusts, or entities have been added

- children’s roles in the business have changed

- one heir has become more active in the business than others

- debt, guarantees, or banking exposure has changed

- parents, founders, or key decision-makers are ageing

- spouse security requirements have changed

- family branches have expanded

- existing documents are older than 3 to 5 years

- old insurance or liquidity arrangements no longer match the current scale of the family

- past planning was done for a smaller balance sheet, simpler family structure, or earlier stage of business

Planning is not a one-time event. As wealth, family roles, ownership, debt, liquidity, and succession realities change, continuity capital must be reviewed.

The purpose is not to criticize earlier planning. The purpose is to test whether the current structure still works for the family’s present scale.

For Existing Clients If we have worked together earlier, this review is not about starting again. It is about checking whether earlier arrangements still match your family’s current reality. As businesses grow, children mature, assets change, debt exposure shifts, and family responsibilities evolve, continuity capital must be tested again. The question is not whether something was done earlier. The question is whether it still works today. |

For Families Exploring This for the First Time This is not a product discussion. It is a private review of whether your family’s wealth can produce usable capital when continuity is tested. The first step is not to select an instrument. The first step is to understand the capital need, timing, control implications, advisor coordination, and implementation risk. |

How Existing Advisors Are Protected

The Continuity Capital Review is designed to work with the family’s existing CA, lawyer, banker, trustee, investment advisor, insurer, and other professionals.

The objective is not to replace professional advisors or disturb existing relationships.

The objective is to create one continuity capital map so that liquidity, ownership, tax treatment, legal documents, family intent, banking arrangements, and implementation steps do not work against one another.

Where technical advice is required, implementation should remain coordinated with the family’s qualified professional advisors.

When Referrers Should Raise This

For CAs: when the client is tax-compliant but transition liquidity is unclear.

Useful referral sentence: “This may not be only a tax issue. It may be worth asking Sandeep to review whether the family has enough continuity capital if transition creates liquidity pressure.”

For lawyers: when documents are being drafted but the funding required to make the structure work has not been reviewed.

Useful referral sentence: “Before finalizing the documents, it may help to review whether the family has the capital needed to implement the structure during transition.”

For private bankers: when the family has assets, investments, and credit relationships, but no transition-liquidity architecture.

Useful referral sentence: “You have strong assets. It may be useful to review whether liquidity, control, and succession are aligned for continuity.”

For business network leaders: when a founder has built substantial value but has not clarified what capital must be available if control changes.

Useful referral sentence: “You should speak to Sandeep. He helps business families review whether wealth is continuity-ready, including whether capital will be available when transition tests the structure.”

What This Review Is Not

The Continuity Capital Review is not:

- an insurance sales meeting

- an investment product comparison

- a loan recommendation exercise

- a tax shortcut

- a legal drafting service

- a generic financial planning review

- a return-maximization exercise

It is a structured review of how capital should be arranged to support family continuity, control, liquidity, fairness, and implementation.

What the review may produce

Depending on suitability and scope, the review may produce:

- Continuity Capital Gap Summary

- Asset Convertibility Map

- Continuity Capital Cascade

- Family Liquidity Policy Notes

- Advisor Coordination Priorities

- Funding Method Suitability Review

- Implementation Sequence

What Happens After the Review

Depending on the findings, the next steps may include:

- continuity capital gap sizing

- family liquidity policy

- Continuity Capital Cascade design

- review of existing cash, investments, reserves, credit, and insurance

- estate equalization funding review

- spouse security review

- business stabilization capital review

- trust funding review

- debt and guarantee exposure review

- advisor coordination meeting with CA, lawyer, banker, trustee, or other professionals

- documentation alignment review

- implementation sequence

- risk-transfer evaluation where suitable

- updated continuity capital plan for the family

The review may confirm that existing arrangements are adequate.

It may also show that arrangements are insufficient, outdated, misaligned, inaccessible, or not suitable for the family’s current scale.

The objective is simple: to ensure that capital is available before the family needs it, not after pressure has already arrived.

Frequently Asked Questions

Is Continuity Capital Review an insurance review?

No. It is a review of the capital required to protect continuity during transition. Insurance may be one possible funding method, but it is considered only after the capital need is clear.

Can existing assets solve the liquidity need?

Sometimes. The review examines existing cash, investments, reserves, credit access, asset-sale capacity, business liquidity, trust assets, and existing risk-transfer arrangements before considering additional instruments.

Are products other than life insurance considered?

Yes. The review may consider reserves, investment liquidity, bank facilities, asset-backed borrowing, trust funding, shareholder arrangements, structured income tools, planned asset monetisation, and other suitable instruments.

When is life insurance relevant?

Life insurance may be relevant when the family needs funded liquidity at a defined transition point and cannot depend on asset sale, borrowing, or business cash flow.

Does this replace my CA, lawyer, banker, or trustee?

No. This review is designed to coordinate with them. Capital planning must be aligned with legal documents, tax treatment, banking arrangements, trust structures, ownership, and family intent.

Should this review happen before or after estate planning?

Ideally, it should be connected to estate planning, succession planning, trust planning, and family governance. Documents and capital should support each other.

Is this suitable for every family?

No. It is most relevant for families where wealth, ownership, liquidity, business interests, family branches, or succession issues are complex enough to require structured review.

Before transition tests the structure, review whether capital is ready.

If your family is asset-rich, business-heavy, real-estate-heavy, promoter-led, multi-entity, or succession-sensitive, continuity capital should not be left to assumption.

The family may have enough wealth.

The real question is whether capital is available, accessible, controlled, and aligned when the family needs it most.