Life insurance alone may safeguard your family’s finances, but assigning policies to a trust transforms protection into precision. For HNIs, CEOs, and family patriarchs in India, combining insurance with trust structures ensures your objectives—education, maintenance, charity, and debt settlement—are honored exactly as you intend.

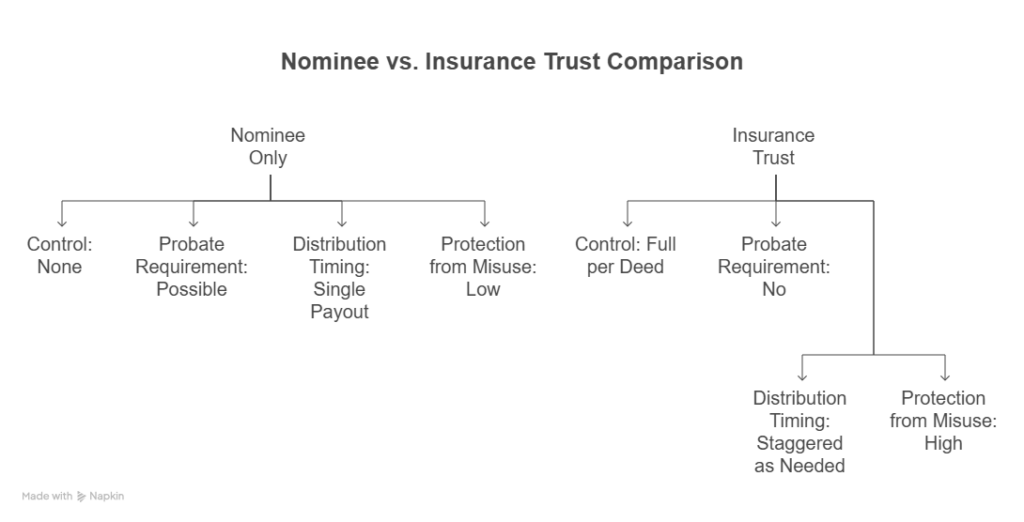

Why Nominees Fall Short

Challenge: Direct payouts to nominees offer no control over post-claim disbursements. Funds meant for a child’s overseas education may be diverted for unrelated expenses.

Example: Without a trust, a ₹2 crore payout to Mrs. Kapoor could be used for personal ventures, not her son’s MIT tuition.

Solution: Assign your policy to an Insurance Trust, a legal entity that mandates distribution per your instructions.

1. Indian Case Snapshot: Chennai’s Rao Family

Scenario: Mr. Rao (Bengaluru) purchased a ₹1.5 crore term insurance policy in 2016. He assigned it to a Minor Beneficiary Trust with a clause:

- Purpose: Oxford University tuition (estimated £300,000).

- Distribution: 25% at admission, 50% in annual installments, remainder at age 25.

Outcome: Upon his death in 2021, the INR-₹1.5 crore (US$200,000) payout landed in the trust within 10 days, funding tuition without delay and ruling out probate.

Impact: Trust-controlled disbursement prevented misuse and covered living expenses (₹12 lakhs/year) seamlessly.

2. Quantified Impact: Trust Benefits in Numbers

- Speed: 7–10 days claim settlement vs. 6–12 months probate delay.

- Tax Efficiency: Death benefits are tax-free under Section 10(10D)—no TDS, no GST.

- Control: Directing ₹50 lakhs for education, ₹30 lakhs for spouse’s maintenance, ₹20 lakhs to charity, ₹10 lakhs for debt repayment—all from a single ₹1 crore policy.

3. Building Your Insurance Trust: Step-by-Step

- Define Objectives: Education, spouse/parent maintenance, charity, debts.

- Choose Policy & Coverage: Term vs. ULIP vs. whole life—align cover ₹ against obligations.

- Draft Trust Deed: Include beneficiary classes, distribution triggers, spendthrift clauses, trustee succession.

- Assign Policy: Execute Form S9 for assignment to trust—notify insurer.

- Review Periodically: Update after births, marriages, wealth changes, or tax law revisions.

4. All Goals, One Trust

An Insurance Trust in India can simultaneously manage:

- Children’s Education & Medical Needs

- Spouse & Parents’ Maintenance

- Charitable Endeavors

- Debt Settlement & Estate Costs

Result: Single governance vehicle, minimal administrative burden, maximal alignment with your legacy.

Key Takeaways for Indian HNIs

- Legal Certainty: Trust deeds trump nominee forms—control is enforceable in court.

- Regulatory Compliance: Assignment aligns with IRDAI regulations and avoids GST on payout.

- Cross-Border Considerations: Nominate NRIs and use FEMA-compliant offshore trusts for global assets.